Aedifica ($AED.BR) is a lesser recognized Belgian healthcare REIT. It operates throughout Europe and boasts enticing fundamentals similar to an 100% occupancy, ~19 12 months WAULT and even a excessive EPRA yield at 8%. But the inventory has been beneath stress since 2021, is that this deserved given the adjustments in rates of interest or does Aedifica presently current traders with a pretty funding case?

Enterprise Profile

Aedifica is a Belgian regulated actual property firm (REIT) specializing within the funding and growth of healthcare actual property throughout Europe. The corporate focuses on senior housing and care amenities, addressing the rising demand pushed by demographic shifts.

Aedifica’s has long-term lease agreements, sometimes with established operators from a mixture of for revenue and non income. The corporate’s portfolio spans Belgium, Germany, the Netherlands, the UK, Finland, Eire and Spain.

Funding case

The funding case is sort of easy for Aedifica, long run tailwinds from an more and more ageing inhabitants throughout Europe supported by a pretty valuation. Let’s break these down:

Demand drivers

The inhabitants in Europe is ageing, the share of these aged 80 years or above within the EU’s inhabitants is projected to have a 2.5 fold enhance between 2024 and 2100, from 6.1% to fifteen.3%. It will require extra ample housing and care amenities which already aren’t maintaining in lots of international locations.

Determine 1: twenty first century growth of inhabitants throughout the EU

Tenants

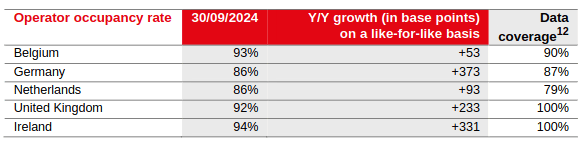

Those immediately taking advantage of the aforementioned developments are the operators of those care amenities. Consider corporations similar to Korian or non income similar to Leger des Heils. They’ve had some after results from covid by means of decrease occupancy, elevated labor prices and better charges. The scenario for Aedifica´s tennants is enhancing although.

Determine 2: Tenant occupancy charges

Yields

As a REIT Aedifica after all may be very depending on rate of interest adjustments, these have an effect on their rate of interest prices and property values and doubtlessly the unfold between borrowing and rental yields. In decrease yield environments Aedifica traded at greater than €120 a share nonetheless as charges elevated the share received minimize in half.

Valuation

As I should not have a crystal ball which incorporates the ECBs charges on the finish of the last decade I valued Aedifica from a state of affairs based mostly method.

Excessive RFR

Base case (present yield)

Low RFR

LTM EPRA yield

10%

7.98%

4%

Present share value

61.90

61.90

61.90

Ending share value

57.43

71.98

143.58

Gathered EPRA per share

24.39

27.10

29.81

Whole

81.83

99.08

173.40

ARR

6.44%

12.01%

36.03%

Desk 1: Quite simple valuation based mostly on 5 years of forecasting, RFR = threat free price

The 4% EPRA yield noticed through the publish covid low yield atmosphere might be repeated once more which in my view shouldn’t be unlikely given the present political scenario in Europe. Even when charges keep the identical to now a really enticing double digit annual return could be noticed. That is based mostly in Aedifica adjusting to increased charges, 2025 and 2026 shall be transitional years on this case. If charges have been to start out rising once more (I’ve doubts the ECB would enhance it way more from current highs) a optimistic return stays because of the excessive EPRA era potential of Aedifica.

Dangers

Charges

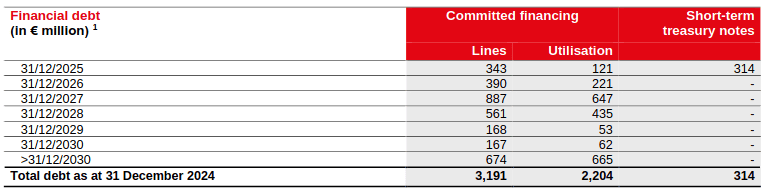

Aedifica ($AED.BR) is rated BBB however considerably increased charges might put stress on them from three sides: decrease asset values, elevated monetary bills and tenant credit score deterioration. Refinancing is unfold out comparatively evenly as debt will get rolled over, quick time period most debt is mounted in any case so most rate of interest adjustments would go into refinanced debt value and hamper development.

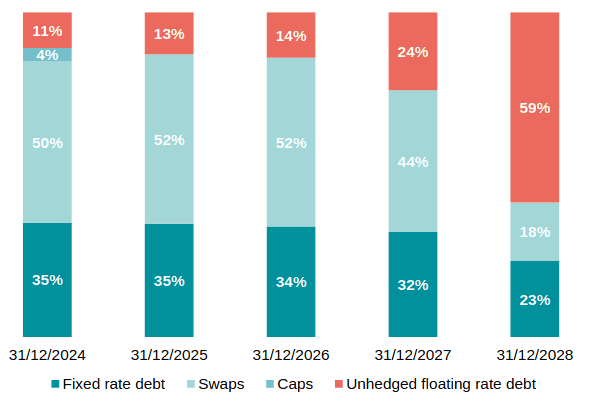

Determine 4: Debt sorts

Demand adjustments

If Europeans handle to stay longer at residence at a price which compensates for absolutely the quantity development in aged this might have an affect on the occupancy ranges of Aedifica´s tenants.

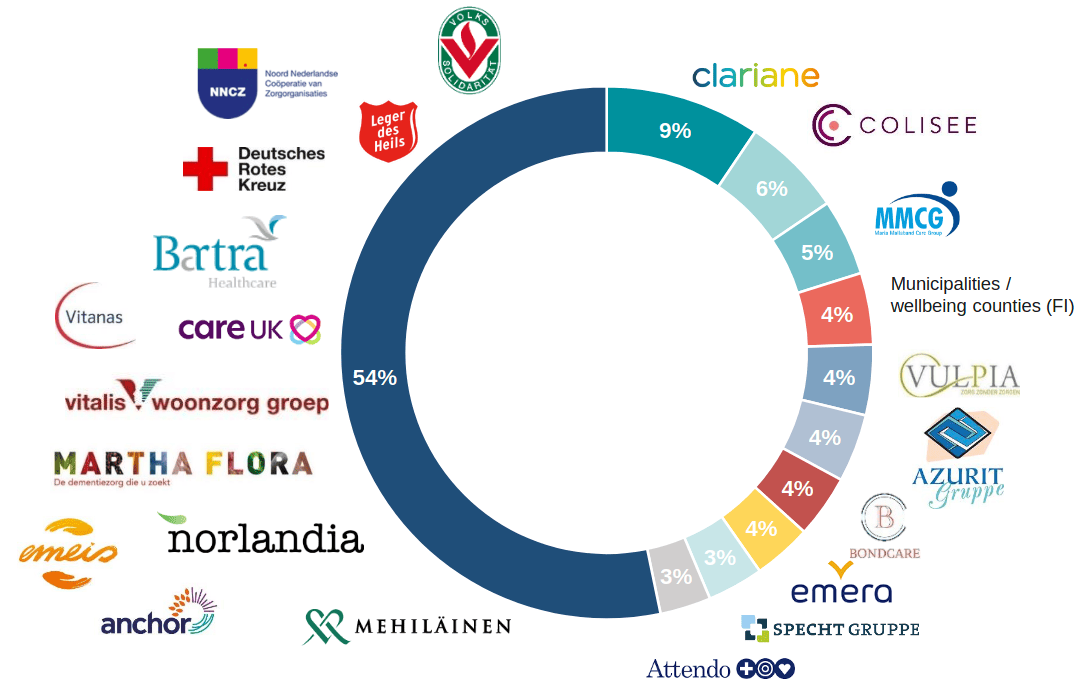

Massive tenants

Aedifica does have some tenant focus with Clariane which is publicly traded and has not carried out effectively, nonetheless their portfolio expansions are additionally diversifying away from massive single tenants and enhance geographical diversification as effectively lowering regulatory threat from sure international locations.

Conclusion

Aedifica presents a compelling funding case with robust fundamentals, together with 100% occupancy (tenant occupancy ~90%), long-term leases (~19-year WAULT), and an 8% EPRA yield. Pushed by Europe’s growing older inhabitants, demand for healthcare actual property is predicted to develop. Regardless of this, the inventory has been beneath stress attributable to rising rates of interest publish covid, impacting valuation. A easy scenario-based valuation implies enticing potential returns even when charges stay regular, with important upside if charges decline and restricted draw back in a barely increased price atmosphere. Dangers embrace refinancing challenges, tenant focus, and potential demand shifts. Total, Aedifica seems undervalued, providing a stable long-term alternative for traders keen to make a directional wager on rates of interest with a top quality firm.

The creator of this evaluation does maintain shares in Aedifica on the time of writing, which can affect the attitude supplied.

This communication is for info and schooling functions solely and shouldn’t be taken as funding recommendation, a private suggestion, or a suggestion of, or solicitation to purchase or promote, any monetary devices. This materials has been ready with out taking into consideration any specific recipient’s funding targets or monetary scenario, and has not been ready in accordance with the authorized and regulatory necessities to advertise unbiased analysis. Any references to previous or future efficiency of a monetary instrument, index or a packaged funding product aren’t, and shouldn’t be taken as, a dependable indicator of future outcomes. eToro makes no illustration and assumes no legal responsibility as to the accuracy or completeness of the content material of this publication.

Sources: annual outcomes 2021, 2022, 2023 & 2024

{kind=link}