Introduction

Crocs ($CROX) is a worldwide chief in informal footwear. The corporate owns the manufacturers Crocs and Heydude, which it just lately acquired. Its administration has made Crocs probably the most worthwhile firm within the trade, even forward of firms like Nike or Adidas. Regardless of this, the market nonetheless doesn’t just like the acquisition of Heydude, which, for my part, will result in greater development and a extra diversified providing of merchandise.

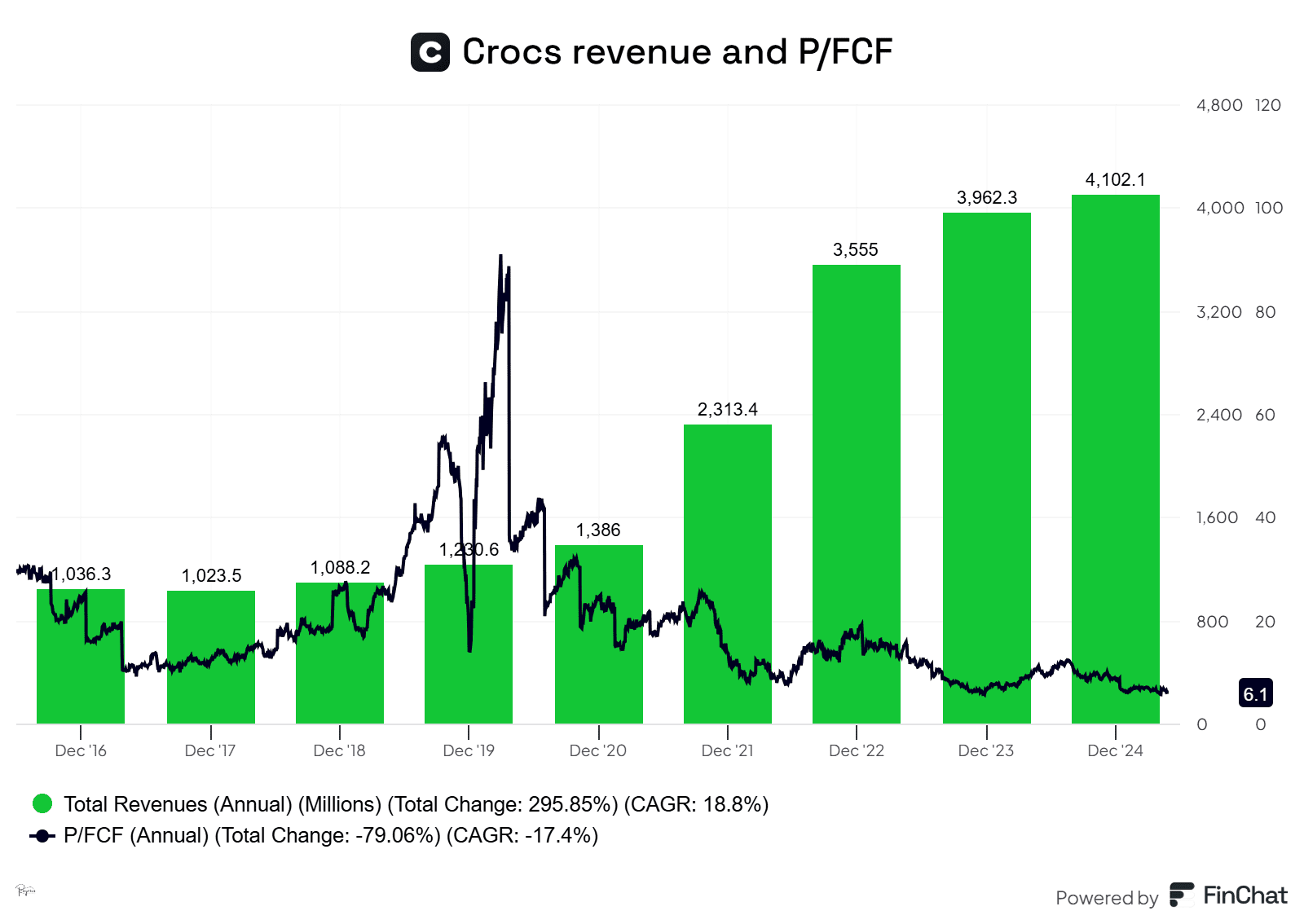

Supply: Finchat, Creator Evaluation

Key highlights

Finest-in-class enterprise valued as a foul enterprise

Good capital allocation and good administration

Heydude, the large situation of the corporate?

Enterprise Mannequin Overview

Crocs’ enterprise mannequin is straightforward: They promote sandals and sneakers, caring for the design, improvement, distribution, and advertising of these sneakers. As said earlier than, the corporate owns two completely different manufacturers: Crocs, which accounts for 80% of the corporate’s income, and Heydude, which accounts for the opposite 20%.

Concerning the Crocs model, its income comes primarily from the US (56%), though the worldwide section of the corporate is rising bigger. Heydude has most of its income coming from the US.

Detailed Funding Thesis

Crocs is presently buying and selling at 6 occasions earnings. With excessive Free Money Circulation conversion and a strong return on invested capital (ROIC), the market is discounting the corporate’s income to fall and its margins to lower. Nonetheless, even when that’s the case for its US enterprise, the corporate is pushing its worldwide enlargement, making room for extra development. Actually, the corporate has steadily been rising its income by double digits throughout the previous.

Supply: Finchat

The corporate has guided for 2025 that Crocs model goes to develop about 6%, whereas Heydude goes to maintain shrinking its income by 7% to 9%. As an mixture, that signifies that the entire firm goes to develop its income by about 3%. Thus, the present valuation is ridiculous since it’s contemplating that the entire enterprise goes to shrink.

Within the meantime, the corporate has accepted $1.3B buybacks, which signifies that the corporate should purchase 20% of its market cap at present below the present authorization whereas paying down debt.

Approaching the valuation conservatively, we are able to worth Crocs as a sluggish grower, with income development of about 3%-4% for the long run. Concerning Heydude, the corporate has pushed an excessive amount of of its sale and is now specializing in a turnaround. The query is, can they do it?

The administration of the corporate has said that it’s following Crocs’ turnaround handbook. They’re making use of the identical measures they took when Crocs’ income fell from 2015 to 2017. For my part, this turnaround can generate headwinds within the brief time period, however from 2026 on, it needs to be accomplished and may add some top-line development to the corporate.

Thus, I assume that this 12 months’s EPS of 15$ per share is sustainable since Crocs’ development ought to offset Heydude’s decline. Making use of a conservative PE a number of of 12 occasions, a lot decrease than its rivals and beneath the common of the US inventory market, the corporate’s inventory ought to double its worth.

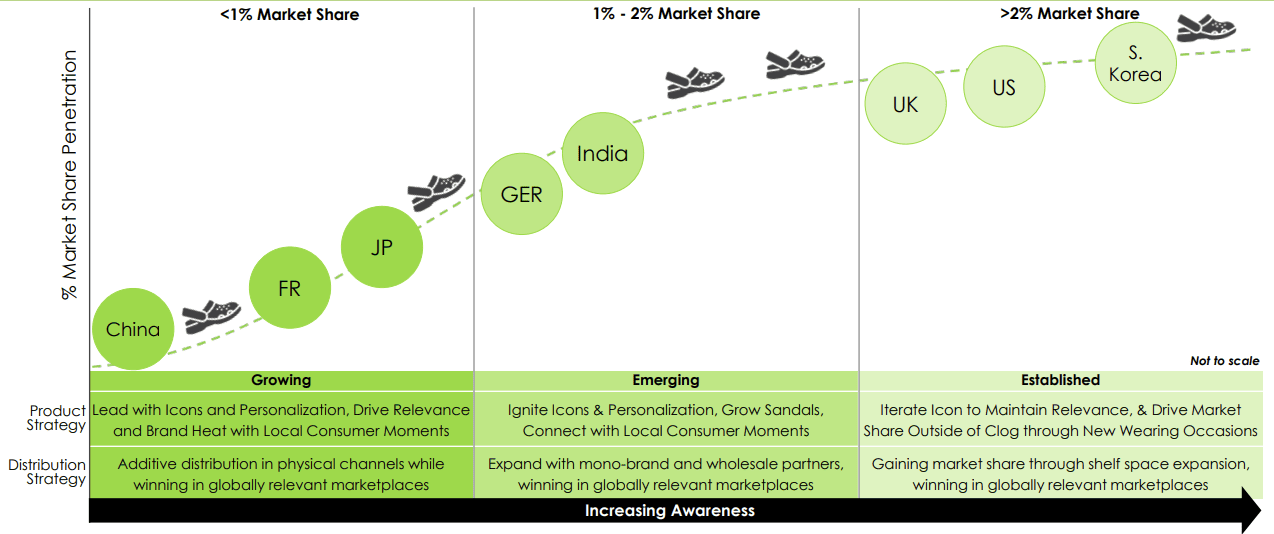

Nonetheless, with this valuation, we go away apart any development that Heydude can doubtlessly generate sooner or later, in addition to any development of Crocs model past 3%. Nonetheless, I think about this situation very pessimistic since Crocs’ worldwide enlargement is concentrating on large economies, like China and Japan, during which the corporate has low penetration of its merchandise.

Supply: Firm’s This fall Earnings Presentation

Catalyst

The corporate has a present buyback program of $1.3B, able to deploy in 2025. It may doubtlessly purchase over 20% of the corporate with the free money move generated in 2025

The development of Heydude’s state of affairs, resuming development, would utterly change the angle of the market. I count on this to occur in 2026.

Acceleration of worldwide development, with a particular deal with China, which is an underpenetrated market with an excellent addressable market.

Conclusion

Crocs is a top quality firm with rational management over prices and a excessive return on invested capital. At present, the market is just not appreciating the worth of the enterprise because of the worry of Heydude’s income lower. Nonetheless, as soon as its income stabilizes, the corporate as a complete shall be rising constantly.

Within the meantime, the depressed worth of the corporate affords the administration a wonderful alternative to purchase again shares at about 6 occasions worth to free money move. I wouldn’t be stunned if all catalysts arrive on the similar time: buybacks and an enchancment of Heydude’s income. This could be a serious catalyst in a really brief time.

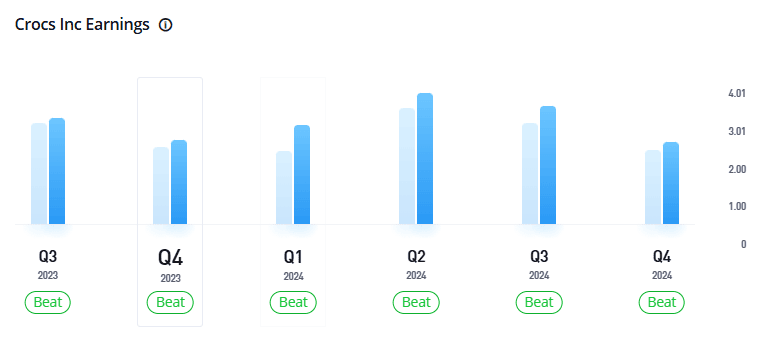

Additionally, the administration is susceptible to attract a worst-case situation to traders. As traders weight these projections to create their estimates, Crocs often beats estimates constantly. Nonetheless, this isn’t taken under consideration in at present’s worth.

Supply: Etoro

At about 6 occasions earnings and free money move, with an enormous buyback program ongoing and whereas rapidly deleveraging, Crocs is without doubt one of the finest choices obtainable to take a position our cash within the US. The worst situation is priced in, leaving room to have a optimistic return in virtually each situation left for the long run.

Threat Components

Incapability of the administration to show round Heydude.

Incapability of the administration to develop internationally.

Slowdown in US gross sales as a consequence of macroeconomic challenges or higher competitors.

Adjustments within the style style of customers, which could be sudden and surprising.

I maintain a place in CROX on the time of writing.

This communication is for data and schooling functions solely and shouldn’t be taken as funding recommendation, a private suggestion, or a proposal of or solicitation to purchase or promote any monetary devices. This materials has been ready with out considering any explicit recipient’s funding goals or monetary state of affairs and has not been ready in accordance with the authorized and regulatory necessities to advertise impartial analysis. Any references to previous or future efficiency of a monetary instrument, index, or a packaged funding product will not be, and shouldn’t be taken as, a dependable indicator of future outcomes. eToro makes no illustration and assumes no legal responsibility as to the accuracy or completeness of the content material of this publication.

{kind=link}