Starbucks has struggled to maintain tempo with the general markets. Will new administration assist? The Every day Breakdown dives in.

Earlier than we dive in, let’s ensure you’re set to obtain The Every day Breakdown every morning. To maintain getting our every day insights, all you should do is log in to your eToro account.

Friday’s TLDR

SBUX has an MVP CEO

However the turnaround will take time

And expectations are climbing

Deep Dive

Starbucks has been battered from its highs, down 30% from its 2021 peak. General, the S&P 500 has achieved fairly effectively in that span, rising about 35%. So whereas shares of Starbucks could possibly be doing a complete lot worse, they’ve clearly underperformed the general market. Will that change going ahead?

New Administration

It was clear that Starbucks was struggling and that its management workforce was flailing, so in September, Starbucks lured away Chipotle CEO Brian Niccol to run the corporate. Niccol value a reasonably penny to usher in — no pun meant — however shareholders have been keen to take the danger.

That’s primarily based on his resume, which features a profitable run at Taco Bell, then jumpstarting Chipotle after a string of food-related sicknesses tarnished its model. Underneath Niccol’s management from March 2018 to August 2024, Chipotle’s income doubled, earnings elevated seven-fold, and the inventory climbed greater than 800%.

The hope right here is that Niccol may also help flip round Starbucks. The truth is that it’ll take greater than 1 / 4 or two to repair.

Progress Expectations

In terms of the basics, there’s excellent news and unhealthy information.

The unhealthy information is, analysts anticipate earnings to fall 26% this fiscal yr — ouch. The excellent news is, Starbucks’ fiscal yr ends in September. The opposite excellent news is that consensus estimates name for 20% earnings development in every of the subsequent two years, and practically 20% development within the third yr.

If Niccol & Co. obtain that feat, the inventory might very effectively be undervalued at at present’s costs.

Dangers

Keep in mind after we did the Basic Evaluation Boot Camp?

Sadly, Starbucks isn’t precisely low-cost at present ranges. At the least, that’s primarily based on its ahead price-to-earnings ratio (or the fP/E), which takes the inventory value (P) and divides it by anticipated earnings (E).

Consider it like this: Even when SBUX inventory value stays flat, a decline in earnings makes the inventory dearer from a valuation perspective.

That is the place buyers should resolve if the inventory is true for them.

The Backside Line

The chance/reward proposition is evident.

On the one hand, you may have a serious potential turnaround within the works beneath confirmed management. If it really works, shares of Starbucks may have notable upside from present ranges. Nevertheless, if the turnaround takes longer than anticipated or doesn’t materialize to the diploma that’s anticipated, then the inventory’s returns could also be disappointing.

It will be much less dangerous to attend and see if the turnaround at Starbucks is taking maintain. Buyers who wait danger having the inventory rise in anticipation of this improvement, then are pressured to purchase in at increased costs (albeit with extra potential stability within the fundamentals). On the flip aspect, those that purchase in early stand to profit probably the most if the turnaround succeeds. However additionally they stand to danger extra if the inventory comes beneath strain.

Wish to obtain these insights straight to your inbox?

Enroll right here

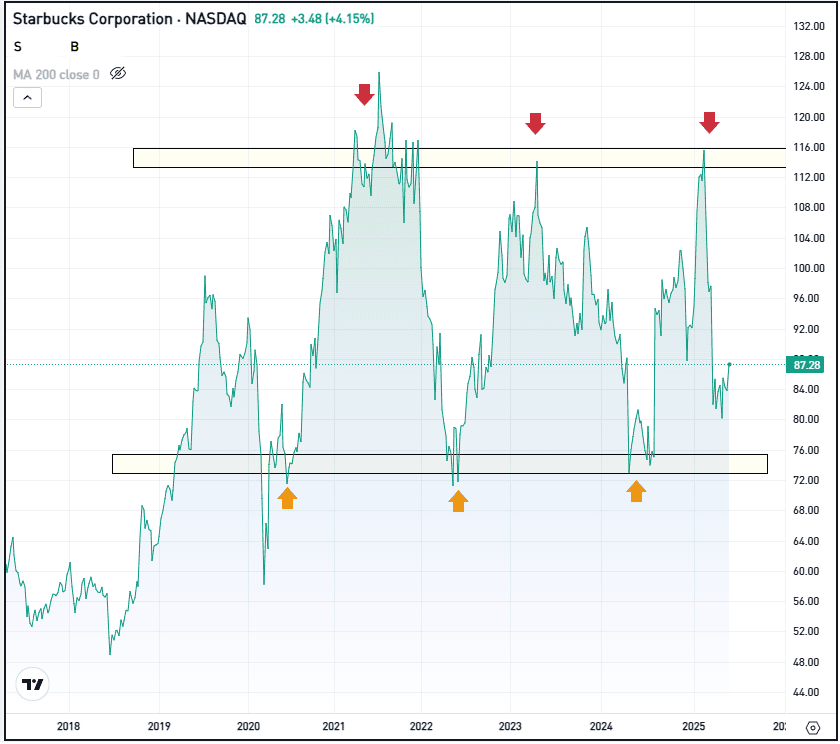

The Setup — Starbucks

Starbucks shares popped from the mid-$70s in August on information of Niccol’s rent and rallied all the best way to $117.46 in March 2025 — lower than 10% from all-time highs. Nevertheless, the pullback has been swift, sending shares again down into the $70s earlier than the most recent bounce.

For a number of years now, shares have been caught between roughly $75 and $115:

Going ahead, buyers wish to see SBUX discover help within the $70s and finally rebound increased. If help fails to carry, decrease costs could possibly be in retailer, doubtlessly down into the mid-$60s. Nevertheless, if the rebound beneficial properties steam, the $115 vary — which SBUX hit just a few months in the past — could possibly be again in play.

Choices

Buyers who consider shares will transfer increased over time might contemplate collaborating with calls or name spreads and might use long-dated choices to take part. If speculating on a long-term rise, buyers would possibly think about using sufficient time till expiration.

For buyers who would somewhat speculate on the inventory decline or want to hedge an extended place, they may use places or put spreads.

To be taught extra about choices, contemplate visiting the eToro Academy.

Disclaimer:

Please word that on account of market volatility, a number of the costs might have already been reached and situations performed out.

{kind=link}

Discussion about this post